Where Has All My Profit Gone?

As accountants we are often asked “how can I have made a profit when I don’t have that much money in my bank account?”

Profit does not equal cash. Profit is sales less expenses. But there are other amounts that come into and out of your bank account other than sales and expenses. For example, tax payments, personal drawings, investment in new equipment, payment of loans.

To better understand where your money has gone, it is better to look at a cashflow statement – what are the cash inflows and outflows.

Cash inflows include:

- Payment from sale of goods and services

- Payment from the sale of business assets

- New loans

- Personal money being put into the business

Cash outflows include:

- Payment of suppliers

- Payment for new equipment or stock that has not been sold yet

- Tax payments

- Personal spending

- Loan repayments

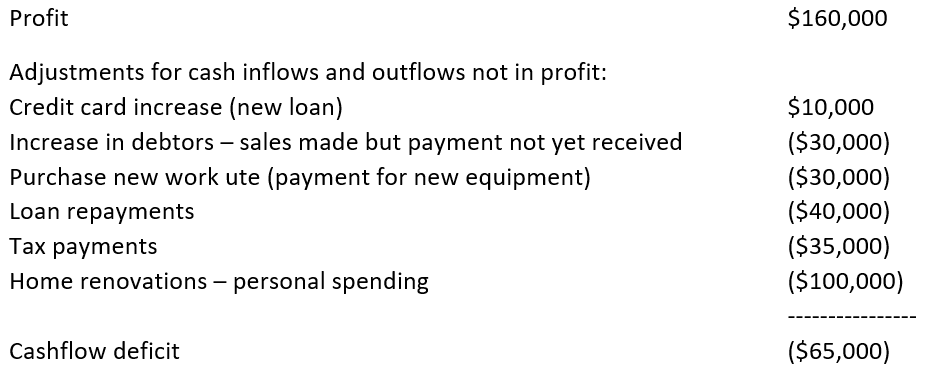

Let’s look at an example:

While the profit for the year was good, there were a lot of cash outflows that are not represented in the profit and loss and have resulted in a rather large cashflow deficit. If there were not sufficient funds in the bank at the beginning of the year to fund this deficit, it would mean you have gone into overdraft. If this situation continues, you will find your business in a serious cash shortage.

What can you do to manage and improve your cashflow:

- Improve your profits – review your margins (are you covering all your costs or have expenses gone up and you have not passed those increases on?), review your expenses (are you paying for subscriptions you don’t use, can you get better terms from different suppliers?). How can you sell more?

- Have a budget for your business – profit and loss and cashflow. Track and understand differences so you can learn, improve and make changes.

- Review your stock holding. Do you need to have as much inventory? How quickly can you get stock in if needed rather than buying it just in case?

- Review your debtors. Follow up customers who have not paid. The longer they take to pay, the less cash you have.

- Review your supplier trading terms – can you delay payment of suppliers – but be aware that this can snowball into amounts that might not be manageable.

- Will refinancing reduce your loan repayments? Can you get a better deal? Be aware of the costs of refinancing – application fees and longer terms may end up costing you more in the long term.

- Plan for your tax obligations – put funds aside for your GST, PAYG, income tax and even employee superannuation so that you don’t spend it on something else.

- Finance new equipment rather than using available cash. However, be aware of the costs of financing.

- Look at your personal spending out of the business. As well as a budget for your business, you should have a budget for your personal spending. Rather than taking adhoc amounts from the business which add up rather quickly, work out what you need and take a regular drawing to live on.

If you wish to look at where your profit has gone and discuss how forecasting and budgets can improve your cashflow management, please contact our office on 1300 620 345.