Fuel Tax Credit Changes

The excise and excise equivalent customs duty rates have halved for petrol, diesel, and all other petroleum-based products except aviation fuels. This temporary reduction is in place for 6 months and applies from 30 March 2022 until 28 September 2022.

Here’s what you need to know when claiming fuel tax credits on your business activity statement (BAS):

- Rates changed on 1 February and 30 March. If you lodge quarterly, 3 different rates may apply to your BAS, which was due on 28 April. Rates are based on when the fuel was acquired.

- The ATO’s fuel tax credit calculator makes it easier for you to apply the right rates.

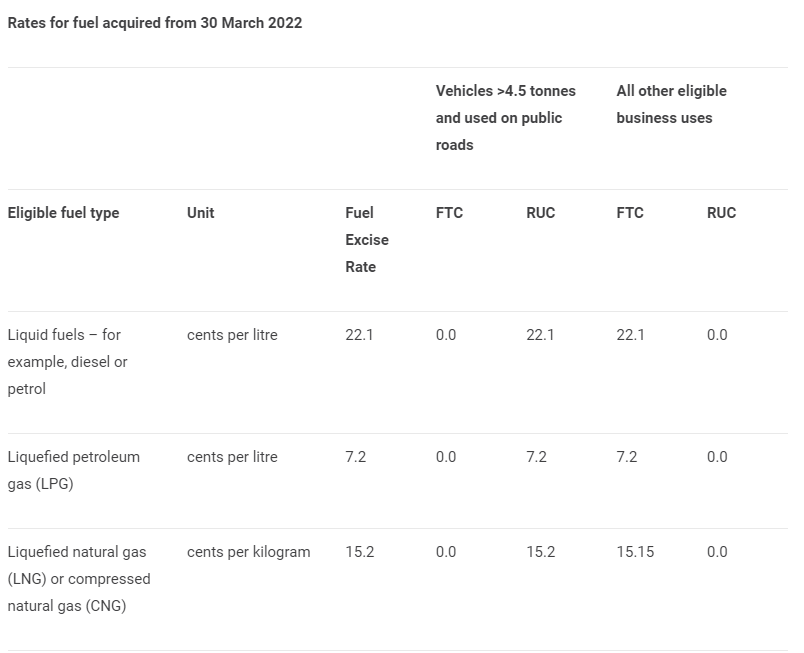

- In this 6-month period from 30 March 2022, businesses using fuel in heavy vehicles for travelling on public roads won’t be able to claim fuel tax credits. This is because the road user charge exceeds the excise duty you’ll pay, and this reduces the fuel tax credit rate to nil.

- The fuel tax credit rate for all other eligible business uses have been halved to match the reduced fuel excise rates.

- It’s important to keep accurate records to support your claims. These records need to show the type, date and quantity of fuel acquired for business activities.

- The fuel excise and fuel tax credit rates will return to normal on 29 September 2022.

Please see the below tables illustrating the changes to Fuel Tax Credits (FTC) rates and subsequent Road User Charge (RUC) borne by businesses (based on the main types of fuel used), in light of the temporary halving of the fuel excise rates from 30 March 2022:

If you have questions in relation to the above, or any other matters, please do not hesitate to contact our office on 1300 620 345.